State Bank of India (SBI), the nation’s largest lender by assets, announced its Q3 FY26 results on February 6, 2026, showcasing impressive growth amid a resilient economy.

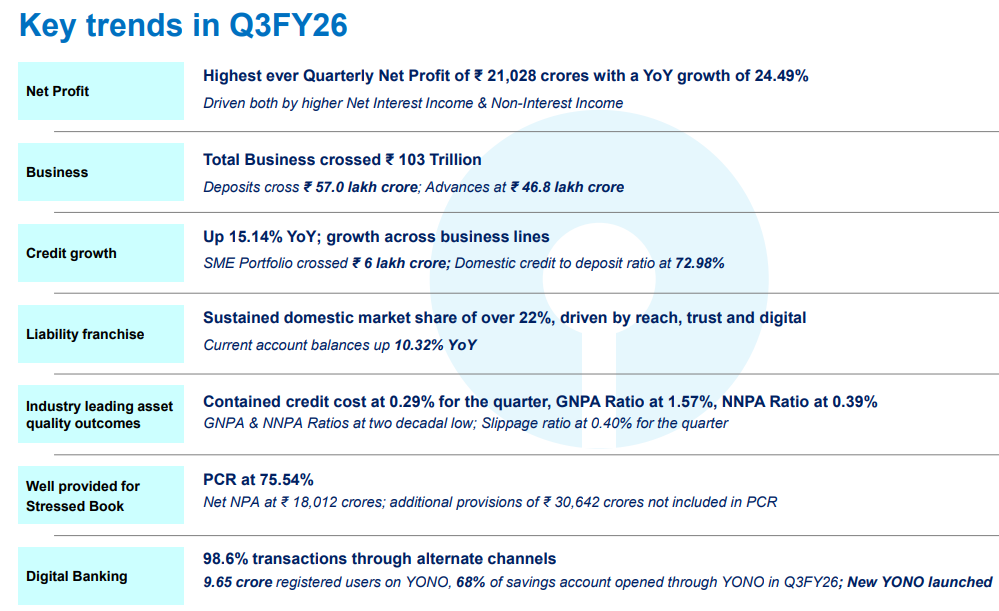

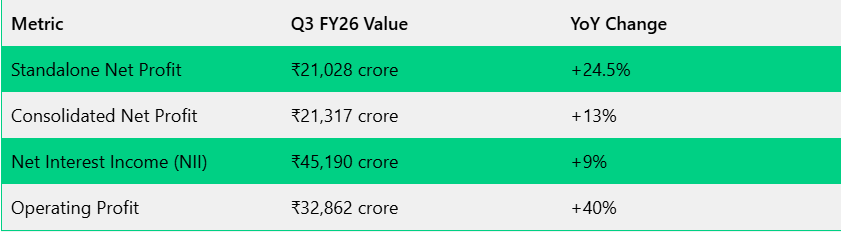

Standalone net profit soared 24.5% year-on-year to ₹21,028 crore, surpassing market expectations and highlighting the bank’s operational efficiency.

This strong performance was fueled by higher interest income, controlled provisions, and robust loan expansion, positioning SBI favorably in India’s banking sector.

SBI’s results reflect a balanced growth strategy, with retail loans surging 16% YoY, SME advances up 21%, and corporate lending at 13%. The bank also upgraded its FY26 credit growth guidance to 13-15% from 12-14%, signaling confidence in sustained momentum despite global headwinds.

The loan book expanded significantly to ₹46.8 lakh crore, driven by strong demand in retail and SME segments, which now form a larger share of the portfolio.

Deposits grew steadily at 9% YoY to ₹57 lakh crore, with CASA ratio holding firm, supporting liquidity and NIM stability at 3.12% domestically.

Asset quality strengthened further, as the gross NPA ratio dropped to a multi-year low of 1.57%, aided by effective recovery mechanisms and lower slippages. Provisions declined notably, freeing up capital for growth initiatives while maintaining a robust CAR of 14.05%.

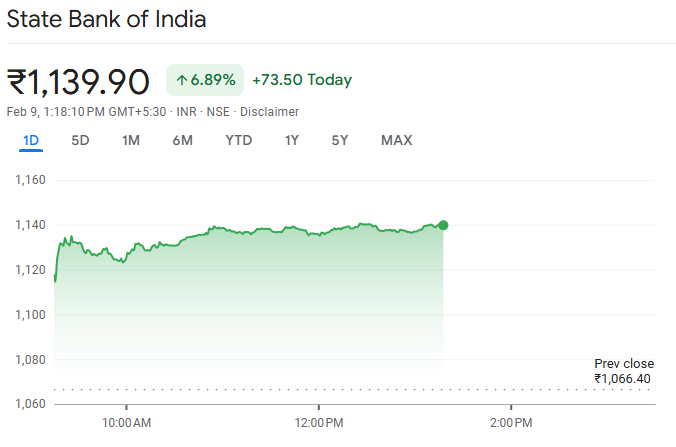

On February 9, 2026, at around 01:18 PM IST, SBIN shares were trading at approximately ₹1,139.90 on the NSE, marking a sharp 6.89% intraday gain.

The stock hit a record high following the results announcement, with gains extending over 7% in prior sessions amid heavy buying from institutional investors. This rally underscores market approval of SBI’s earnings beat and positive guidance.

SBI’s performance benefited from India’s steady economic recovery, rising credit demand, and prudent risk management. Retail and digital banking segments shone, with fee income rising and non-interest income contributing to operating profit growth of 40% YoY.

However, potential risks include NIM pressure from deposit rate hikes, regulatory changes, and global uncertainties affecting corporate lending. Management remains optimistic, targeting 9-10% deposit growth for FY26.

SBI’s Q3 FY26 results demonstrate operational excellence, with record profits, cleaner books, and ambitious guidance reinforcing its top position in Indian banking. Investors tracking PSU banks should consider adding on dips, as the bank’s growth trajectory aligns with India’s economic upcycle.

Source: SBI Investor Presentation

Open Free Demat Account!

In just a few minutes, Simply provide some basic personal details, to get started.

About | Research | Pricing | Upcoming IPOs | Blog | Become a Partner | RMS Policy | Privacy Policy

Fund Transfer for Trading | Fund Transfer for DP | Client Back office/DP Login | Partner Login | Buy-Back | Margin Calculation | Re-KYC | Downloads | Platform | Loans

CIN - U65921WB1994PLC217071 | SEBI Registration No. INZ000169130 | DP SEBI Reg ID : IN-DP-533-2020 | CDSL : 1234500 | NSDL : IN303591 | Member ID`s : NSE - 08334, BSE - 912, MSEI - 18300, ICEX - 1133, MCX - 56415, NCDEX - 1286 | AMFI : ARN-12417, Date of Initial Registration: 21.10.2003, Valid Till – 21.11.2028 | APMI registered PMS Distributor, APMI APRN: 08501 | Research Analyst : INH000000206

Trinity, 226/1, A.J.C. Bose Road, 7th Floor, Kolkata - 700 020, India.

**Investments in securities market are subject to market risks, read all the related documents carefully before investing.